Analysed: Why the “Uber for Trucks” model might be broken

Navigating key supply and demand side challenges on the road to success

In Silicon Valley there is a particular way of describing new companies that goes something like this: “Our company is the [insert FAANG or well-known tech company here] of [insert industry or sector here].”

A cursory glance at the info section of Y-Combinator’s latest batches has: Amazon for Construction (CostCertified), Google Analytics for the Physical World (Zensors), and LinkedIn for skilled blue-collar workers (PowerUs).

One now well-worn combination would certainly be “Uber for Trucks”. Where Uber matches drivers with riders, “Uber for Trucks” (or Logistics-as-a-Service) promises to match trucks with shipments.

2021 saw a spate of truck-capacity sharing platform activity. Chinese company Manbang’s successful IPO gave it a valuation of $20bn. DiDi Chuxing (the company which has earlier taken-over Uber’s operations in China) increased the breadth of its cargo transport services to 10 cities across China. And Uber itself has been busier than ever through its Uber Freight unit, having entered into a commercial pilot with self-driving truck company Aurora to haul goods for customers in Texas.

2021 was also a year in which supply chain challenges became more publicly visible than ever before. As lockdowns lifted, demand rocketed. Supply chains that were disrupted during the global health crisis struggled to bounce back, and this led to chaos for the manufacturers and distributors of goods, unable to produce or supply as much as they did pre-pandemic for a variety of reasons including worker shortages and a lack of key components and raw materials.

So, does this not mean that the stage should be perfectly set for the “Uber for Truck” businesses to, in the words of meme stock traders, go “to the moon”?

And yet, there is something inherently broken about the Uber for Truck business model. Here’s why...

What is logistics like now, and what constitutes logistics-as-a-service (LOGaaS)?

To start with, let’s consider why logistics matters to FMCG companies. In part because it is a cost-driver. Historically not a significant one, but a driver none the less (as this graphic illustrates, it is around 6 cents per $2 spent on a can of Coca-Cola).

However, the main importance of logistics is not in its cost, but in the cost of its failure. Let us assume that a customer would order a product for which they charge $2 at retail. The logistics cost component of that is relatively small. But a failure in that portion of it would crash the sale. In extreme but certainly not unheard of scenarios, failure to supply product could result in cancellations of large promotions or a switch to rival brands.

In order to ensure stability on delivering against base volume forecasts, large FMCG companies enter into contracts with large 3PLs (third party logistics providers). To secure this fixed capacity for certain transport lanes on the logistics network, contracts have minimum commitments from both sides. On the part of the FMCG manufacturer, this would normally be agreements on volumes to be delivered and transport lead time provision, particularly along major routes. On the part of the 3PL, these would be truck availability and adherence to ordering process + proof of delivery criteria.

So whilst such negations drive stability for core volumes on both sides, it is clear that for FMCG companies the ability to more dynamically arrange logistics from point A to point B at shorter notice and for lower volumes would be great, and for 3PL companies the ability to make use of the current empty space they have transporting loads would be a game-changer. This is where logistics-as-a-service may have a role to play.

Logistics-as-a-service falls under the branch of business models known as marketplaces, and there are conventionally 3 parties in such a model:

Supplier = trucks with excess capacity

Distributor = the logistics-as-a-service platform

End-User = shipments that need to be moved

For the sake of simplicity of this analysis, we will focus on the supply-side and end-user side for now.

Let’s even assume for a second that the platform itself would be perfectly optimised, and ideally would demonstrate some of the following traits:

Helps to connect truck drivers with cargo owners through an easy to use mobile platform

Improves freight efficiency and lowers empty-load rates for truckers by using great algorithms to ensure correct driver + shipment matching and allocation

Has route tracking + proof of delivery functionality built-in (this is a key artefact needed to force payment from the buyer of the shipment)

Even with this perfect platform, there are still some inherent operating model problems on the supply and demand side which to my mind provide challenges that cannot be easily overcome.

What are the differences between transport-as-a-service (eg. Uber) and logistics-as-a-service (eg. Uber for Trucks)?

For all the doubts about what market capitalisation a company like Uber, with a track record of one loss-making quarter after another, should have, there is one thing which can be said about Uber: that is has made itself a key part of life in Western cities, and has a robust group of suppliers (drivers) and end-users (passengers).

Yet there are some key differences between it and what a logistics-as-a-service model portends.

Key Difference 1: Spare Capacity through Existing Assets on the Supply Side

Let’s think about the three distinct stages of the development Uber on the side of the driver side (supply-side)

Step 1: People who already own their own assets (cars) take up driving part time as a way of earning some extra cash

Step 2: Uber takes off and gains sufficient volume of passengers to the extent that some drivers are able to use it full time

Step 3: Uber becomes so big that the market is able to support more than one-player, and the rush of invested capital in the business model means that it might make sense to app-switch to get the best rate per mile (Eg. Some drivers using bother Lyft and Uber)

By the time the business model has reached Step 2, it is clear that the business is viable. By this step, it has product-market fit on both the demand side and the supply side.

However, it is only possible to reach Step 2, where lots of passengers come on-board and the demand side is built up because of what happens in Step 1, which is where the supply side is built up by new drivers coming into the availability pool. For standard car drivers, it makes sense that many would be able to drive their cars to make some extra cash but for trucks, is this going to be the same situation?

Very few people just have a truck parked outside their house, sitting there with excess capacity ready to be used. Incidentally, private truck ownership is more common in China and perhaps partially explains Manbang’s valuation, but in Western markets that would not be the case. The trucks which are available tend to attached to already large 3PLs.

And whilst we contended above that 3PLs might be keen to use the excess capacity they have, let us not forget that the world’s major logistics companies spend cash on marketing precisely to drive a value proposition in which shipping is not just a commodity!

If we think of the yellow New York Taxi or the London black Cab as the DHL or FedEx of the old world, they were the non-commodity item. It was only through the emergence of Uber that a journey became commoditised, and ultimately as Uber Pool and other services were introduced, the passenger also became a standardised unit.

There have been examples of the logistics industries standardizing or commoditising itself- the prevalence of the shipping container as we know it today came about through one company releasing their patents, thereby bringing about standards in every aspect of containers from their overall dimensions to how they can be stacked, to the twistlocks that securely fasten them to ships. But that was in an era when cross border trade was relatively negligible and even having a small part of a growing market would have been better than standing still.

Yet when it comes to logistics-as-a-service, from the perspective of a 3PL releasing capacity onto a platform, it would seem to only further drive their own commoditisation and margin erosion in a world which is perhaps already as globalised as it can be.

To summarise, in order for there to be the requisite unlock on the capacity side, we can see that there would need to be either:

a majority of small truck drivers owning their own trucks and/or having the ability to do trucking on a freelance basis

or major logistics companies which do currently have the capacity needed would need to be prepared to commoditise themselves

…and it seems like neither of these currently or imminently will exist on a structural basis.

Key Difference 2: Cost of Failure on the Demand Side

Turning now to one of the key demand-side differences: let’s once again start by taking Uber as an example.

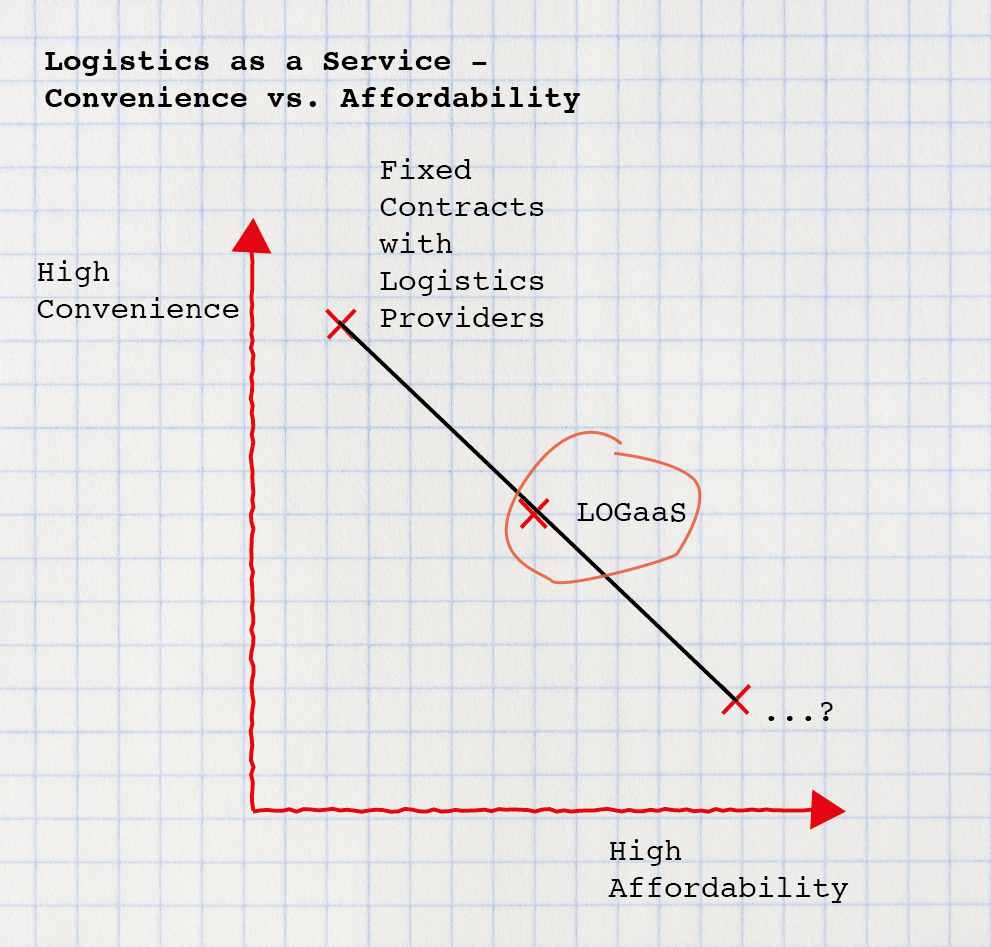

When it comes to taking transport, clearly there is a constant trade off between affordability and convenience.

We can see in this scenario that where the consumer may previously had a binary choice of

Low-affordability and high-convenience: private taxi

High-affordability and low-convenience: public transport

…there is now a third way…

Medium-affordability and medium-convenience: Uber

But if that third way doesn’t work out, they can still take public transport. The economic underpinning of that tends to be paid for by public bodies and therefore sustains it even if volumes dip.

However, what about if we re-work this paradigm for logistics-as-a-service:

There is a low-affordability and high-convenience = fixed contracts with logistics providers.

There would now be a medium-affordability and medium-convenience = Logistics-as-a-Service.

But there is no high-affordability and low-convenience option. There is no public transport of logistics. Maybe you could say that is what publicly supported mail companies are, but this is only for very small loads.

The point is that if the logistics-as-a-service option doesn’t work out and that is what you have banked on, you have problems! The fixed contract option is already not possible because you can’t go back in time to sign that contract. And there really becomes a chance that the load can’t be delivered. And therefore, the cost of failure would start to become unsustainably high.

The circumstances in which Logistics-as-a-Service could work

As far as I can tell, there are only two circumstances in which the core logistics-as-a-service model could work:

Where a certain amount of capacity has already been locked to deliver the core loads, with LOGaaS used for supplementary loads which are not lead time dependent

In markets where truck drivers own their own trucks and work on a freelance basis with existing informal ways of obtaining business, in which case the app connects supply and demand in a more effective way (eg. in China)

But because of the supply-side and demand-side issue mentioned above, I don’t many situations in which it becomes like Uber and upends the previous model.

So where it does work, how can money be generated (value generating activities)?

There are three main ways in which the Logistics-as-a-Service platform provider can make money; assuming that product-market fit is reached on the supply and demand side

Membership Fee

By viewing their role as a gate-keeper to a database connecting existing supply and demand more effectively, a gate-fee may be paid in the form of membership

Brokerage Fee

By viewing their role as a marketplace in which each and every transactions is better facilitated, a cut may be taken from every transaction which connects the truck and the load

Cross-selling Fees

By viewing their role as a trusted industry partner, there are a number of additional fee channels which can be generated through cross-selling

selling top-up toll cards and fuel cards

directing truckers to service stations and receiving commission cuts

helping independent truckers issue receipts to customers

providing insurance services

providing access to second hand truck markets

Depending on what the central revenue generation structure in place is, different incentives would be created in terms of how the business model should focus its development.

If the main revenue is expected to come form membership fees, then the incentive is to grow the user base; whereas if the focus is on taking brokerage fees, the incentive is to grow volume of transactions per user. In early stage of operations, it would be preferable to focus on growing the user base to overcome as much as possible the problems related to liquidity and cost of failure as mentioned above.

For context, Manbang gets 22% of its revenue from membership fees, a mere 0.6% from commissions/brokerage fees, and the rest comes from cross-selling fees and services. Its main revenue comes from the sideline business of helping independent truckers draft and issue receipts to cargo merchants.

What would lead to market dominance for the logistics-as-a-service platforms?

In the above we have reviewed some of the factors for and against the logistics-as-a-service business model. Let’s now focus on what would ultimately lead to market dominance for the platforms themselves.

As mentioned earlier, the goal of these platforms is to commoditise the act of shipping pallet size loads in the same way that ride-sharing companies have commoditised the taxi market.

The overarching idea would be to create a service so reliable that it can be used consistently. As such, key players in the market would work to ensure that prices are similar and that the definitions of units, delivery lead times etc. are consistent.

This would make the primary means of differentiation truck liquidity, which would over time work in favour of the bigger platform. It is reasonable to assume that eventually the majority player would become dominant - with greater usage both on the side of the trucker and on the side of the person who wants to deliver a load. This would particularly be the case if there were forced exclusivity arrangements (Eg. one trucker can only be on one platform at a time).

If we look at China as a case study of the eventual tilt to dominance which comes from having high supply or demand - Didi entered the market after Manbang, but is now growing faster. It’s edge lies in the fact that is has about 550 million registered taxi users on its platform (about 1/2 of the Chinese population!), which in turn can boost demand for services such as home-moving, a typical use scenario for truck-hailing.

Demand-side advantage will eventually also create supply-side advantage with truckers realising Didi is where they can get the most delivery jobs. And in turn this increased liquidity on the supply-side will then lead to more numbers on the demand-side, leading ultimately to market dominance.

So where does this all leave logistics-as-a-service?

We have discussed that there are two structural factors which work against logistics-as-a-service - namely the difficulty in building up liquidity on the supply-side and the cost of failure on the demand-side.

Assuming these structural factors are overcome, we can see that there are three possible sources of income: membership fees, brokerage fees, and cross-selling fees. Depending on where most money comes from, the relative incentives of growing the user base or growing the number of transactions would vary.

The one similarity we can see to Uber, and indeed to any marketplace, is that once a dominant advantage in supply or demand-side is built up, a flywheel effect kicks-in, in which more supply leads to more demand, and vice versa.

There is of course one final existential threat which sits above all of this - any form of driverless truck can instantly rebalance the supply-side equation. In this scenario, presumably the route direction software of an incumbent is still significant, but advantages stemming from supply-side truckers becomes less relevant.

Great article! Another challenge to unlocking the capacity required to make the Logistics as a Service model work, is the fact that certain products require special truck types e.g. ambient, frozen, chemicals etc.